[Interact Analysis] Sales of off-highway vehicles will drive electrified components market

As shown in this insight by Jamie Fox, Principal Analyst at Interact Analysis, the soaring demand for off-highway vehicles is creating a strong market for electrified off-highway vehicle components. Global sales of off-highway vehicles are set to increase from 5.6 million in 2022 to 7.2 million in 2030.

As shown in this insight by Jamie Fox, Principal Analyst at Interact Analysis, the soaring demand for off-highway vehicles is creating a strong market for electrified off-highway vehicle components. Global sales of off-highway vehicles are set to increase from 5.6 million in 2022 to 7.2 million in 2030.

Off-highway vehicle sales are predicted to soar from 5.6 million in 2022 to 7.2 million in 2030 and the proportion of fully electric vehicles is increasing, creating a strong market for electrified components.

With strong growth anticipated in the off-highway vehicles market, we predict an increase from a total of 5.6 million off-highway vehicles sold globally in 2022 to 7.2 million in 2030), led by the development of economies in the Asia Pacific region. Forklifts are at the forefront of this growth, with just over half of the total vehicles sold, while scissor lifts and tractors are also contributing high percentages. This makes off-highway vehicles an attractive target for electrification, with growing total sales volumes combined with a growing percentage of electrified vehicles adding up to a strong market for electrified components.

Electrification is much more advanced in some areas than others

Off-highway vehicles were already estimated to be 27% fully electric in 2022, largely due to forklifts (63% electric) boom lifts (25%) and scissor lifts (89%). However, if we exclude these categories, the number of fully electric machines in 2022 was only 0.04%, not even one in a thousand! The figure for all large off-road machinery, such as excavators, bulldozers and large loaders, remains under 1% electric today, so there is a clear division between different types of machinery.

A very good rule of thumb is that smaller machines electrify faster and this is true in the on-road segment as well. Two and three wheelers have electrified faster than cars, cars have electrified faster than SUVs and pickup trucks, while medium and heavy-duty road trucks have had the slowest rate of electrification of all.

This is due to difficulty of design, high infrastructure costs and integration with the grid, economies of scale, and battery weight and cost. Therefore, even if the savings on running costs vs diesel are huge, in practice they can’t yet be realized for larger machinery in most cases. Given this, we forecast that electrification of larger vehicles will continue to take place slowly. Excluding forklifts, boom lifts and scissor lifts, off-road equipment is forecast to grow from just 0.04% in 2022 to 0.27% in 2025 and 5.1% in 2030.

Mini and small excavators are forecast to electrify faster and there are many electric excavators already on sale. At Bauma in October, for example, Caterpillar, Hitachi, XCMG and others displayed numerous electric excavators. These range greatly in size from Hitachi’s 2.3 tonne ZX23U-6EB (10kW motor power, 18kWh battery) to much larger machines such as Komatsu’s 24-tonne, PC210 Electric (123kW, 451kWh). However, while many excavators have been launched, actual shipments are slow and in practice most available models are mini or small excavators.

Over time, excavators and tractors will add considerably more component revenue. In the case of tractors, this is because there are so many tractors that even a small portion being electrified will add significant revenue.

60V and under dominates off-highway electrification

Almost three-quarters (74%) of electrified machines were 60V and under in 2022, largely because so many machines are forklifts, which are often low voltage. The 74% is forecast to hold steady until 2027 and then decrease slightly to 71%, as larger machines, which use higher voltages, electrify. Higher voltages are expected to be common in some machine types, including bulldozers and excavators. Other machine types, such as loaders and tractors, are forecast to use a range of different voltages. Higher voltages (500-1,000V) are currently more commonly found in diesel-electric vehicles, but these voltages are also highly likely to be used in the largest fully electrified battery electric vehicles (BEVs).

Battery pack is largest share of component revenue

Battery packs account for 38% of 2023 revenue in the off-highway electrified components market, followed by 25% for motors and 23% for inverters.

In the off-road vehicles market, the share of component revenue accounted for by battery packs is lower than on-road. This is due to the fact that machines can often be charged on-site and won’t be stranded if they run out of electricity, so there is less margin for error required. Also, some off-highway vehicles are used intermittently during the day, whereas buses and trucks are more commonly used continuously. In addition, low speeds of movement require less stored energy.

Battery pack prices are much higher in the off-road market than on-road due to low volumes and the need for greater customization of different machines, with a typical range of $300-$500/kWh. In some cases, such as forklifts, battery pack prices can be closer to $200/kWh, but in cases of very high-quality, low-volume, specialized designs prices of more than $500/kWh are far from unheard of.

Component prices peaked in 2023

Prices clearly increased from 2020 to 2022 (with the exception of fuel cells), so the interesting question is what is happening in 2023? There was some slight difference of opinion among those we spoke to in order to compile the latest report, but overall a clear picture emerged.

Pricing has reached a plateau and 2023 pricing will be similar to 2022, perhaps a little higher on average in most cases due to pricing being lower at the start of 2022.

Feedback from suppliers – and data gathered – makes it clear prices have been stable in the first half of the year, with similar likely in Q3. Q4 2023 is more uncertain, with suppliers reluctant to give feedback, but we estimate based on fundamentals that it may be the start of a reduction in pricing which could continue into 2024 and 2025.

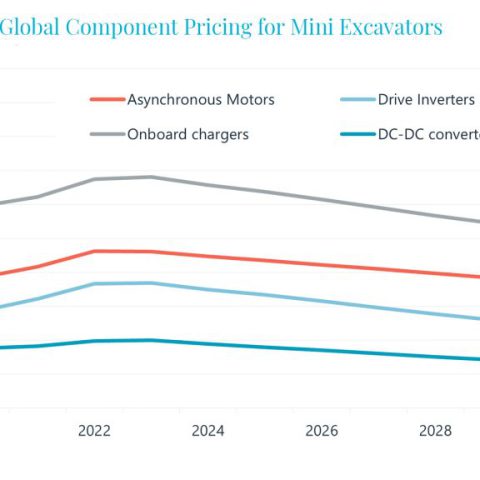

The graph below shows global pricing for asynchronous motors, drive inverters, onboard chargers and DC-DC converters for 2020 to 2030. The full report also includes this data by region, for all other off-highway machines/vehicles, and for other components: PEM motors, work inverters, fuel cell and hydrogen tanks.