CEMA: 2021 tractor market, + 17% increase despite shortage of raw materials

The European Agricultural Machinery Association takes stock of the situation on registrations of agricultural machinery in Europe in 2021, in light of the Ukrainian crisis which has already led to new bottlenecks in the supply of raw materials. The data and graphs

The European Agricultural Machinery Association takes stock of the situation on registrations on the tractor market in Europe in 2021, in light of the Ukrainian crisis which has already led to new bottlenecks in the supply of raw materials. The data and graphs

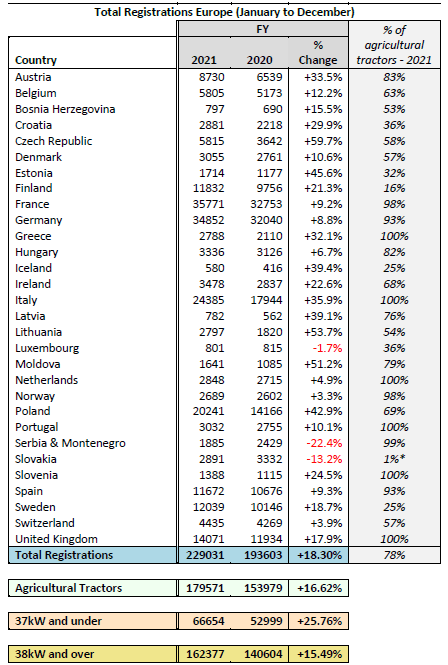

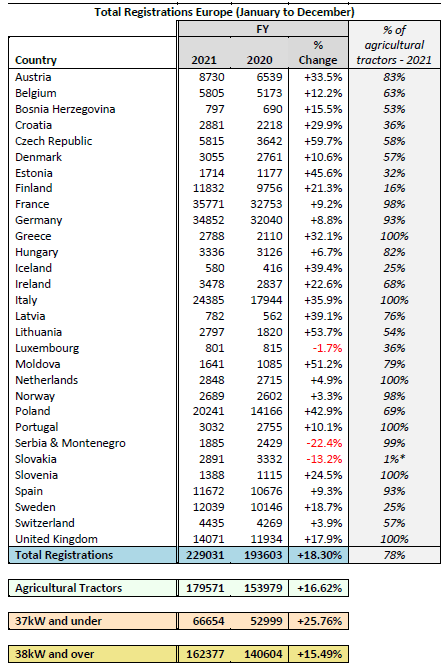

Almost 230,000 agricultural machines registered in 2021, of which just under 30% with powers up to 37kW (50 HP) and 70% above 38kW. With tractors proper at 180,000 units, followed by a variety of vehicles classified, from time to time, as quads, side-by-side, telehandlers or other equipment of various types. The data released by CEMA, or the European Agricultural Machinery Association, on the state of the 2021 tractor market in Europe (whose table with the nation-by-nation trend can be consulted below) are promising data, if we consider the raw material and global supply chain crisis that has afflicted the sector for more than a year which, among other things, are also being affected by the negative consequences of the dramatic ongoing conflict in Ukraine.

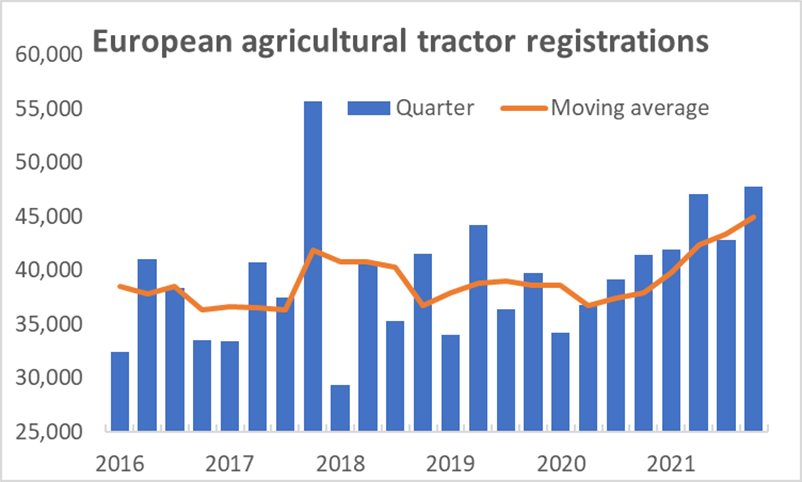

Therefore, as regards the 2021 tractor market, registrations increased by about 17% compared to 2020. Even taking into account the market disruption in 2020 caused by the Covid-19 pandemic, particularly in the second quarter, for CEMA this growth represents a significant improvement in market conditions, with the highest number of tractors registered in ten years. Commendable results achieved despite widespread disruptions to global production supply chains and staff shortages due to the pandemic crisis.

2021 tractor market: well despite the global difficulties

Agricultural machinery manufacturers point out that disruptions to the smooth operation of their production activities have multiplied in recent months. In general, the situation has been worsening since the summer of 2021, well before the crisis in Ukraine. Furthermore, according to what was reported by the CEMA Barometer of February 2022, 51% of the producers interviewed, precisely because of the current crisis in Eastern Europe, said they expected some production interruptions due to shortages on the side of suppliers in the next four weeks. The problem is even more prevalent among tractor and harvesting equipment manufacturers, with 64% and 71% of respondents respectively saying they expect production disruptions (Graph 2). The war in Ukraine has triggered even more supply bottlenecks, as already evident in the latest CEMA Barometer at the beginning of March.

These concerns add to other reported disruptions: transport and logistics, where container shortages have caused a sharp increase in costs and delays; availability of manpower to operate the plants at full capacity due to the spread of the Omicron variant; increased costs of raw materials and energy. As the outages continue to worsen and the agricultural use season is upon us, manufacturers once again stress their concerns about being able to fulfill their orders in a timely manner, despite all efforts being put in place throughout the food chain. value. With the full impact of the war that still remains to be assessed.

Registrations up throughout the tractor power ranges

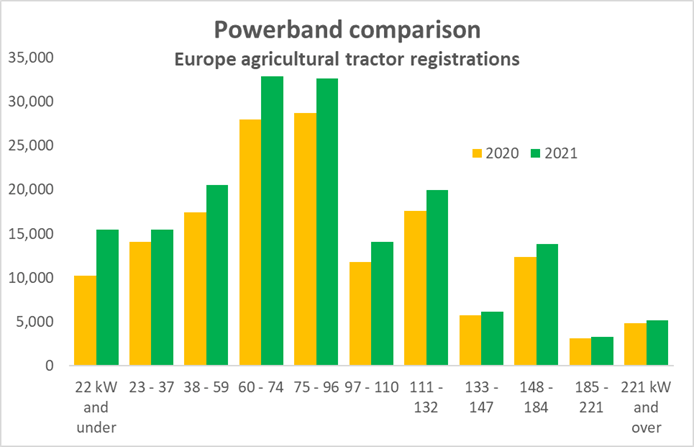

All power categories saw an increase in registrations in 2021, but growth was slower for the larger tractors. Among the machines classified as agricultural tractors, there was a 9% increase in the number of machines above 132kW, half the rate of increase recorded for machines with lower powered engines. The strongest growth of all was for tractors of 22kW or less, with registrations up by more than half from 2020.

The role of commodity prices

While the tractor market was held back by production delays, demand was consistently strong throughout 2021. A number of factors contributed to the level of demand, but the high and rising prices of agricultural commodities were perhaps the most important. This is evidenced by the global food price index published each month by the Food and Agriculture Organization of the United Nations (FAO). This showed that food prices in 2021 were on average 28% higher than in 2020 and were at their highest level since 2011.

Tractor market 2021, the differences between the various European countries

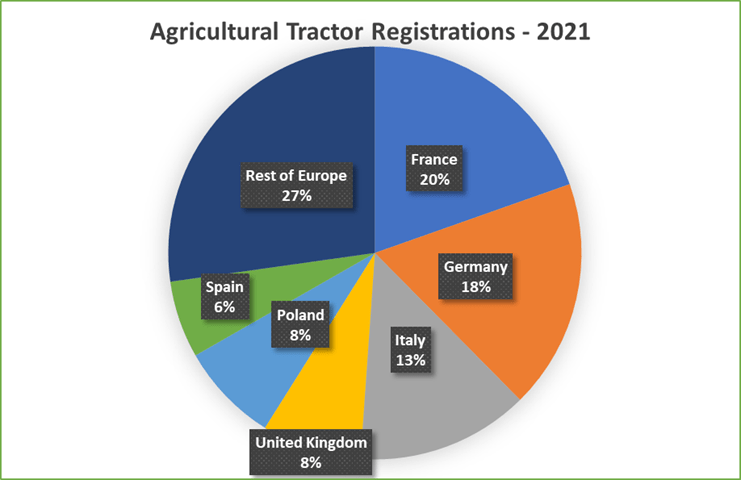

The two largest agricultural tractor markets in Europe remain France and Germany (as can be seen in the pie chart below), countries which account for nearly four out of every ten agricultural tractors registered in Europe. Registrations in these two countries grew more slowly than in the rest of Europe in 2021, however, with increases of 10% and 9% respectively. By contrast, growth in Italy and Poland, the third and fifth largest markets, was particularly strong at 36% and 42%. Together with the UK and Spain, these countries account for a further 35% of European registrations. Just over one in four of the new agricultural tractors registered in Europe are outside these six main markets.

{kind=link}